What Are the Different Credit Scoring Ranges?

By: Jim Akin

Published: July 25, 2019

To interpret your credit score, and what it tells you about your borrowing power, you need to understand where the score falls along the score range between the lowest and highest numbers generated by its scoring system.

All credit scores have the same basic goal: helping lenders (and other potential creditors, such as landlords and utility companies) understand how risky it may be to do business with you. High credit scores indicate a relatively low likelihood of default and relatively low risk for creditors. Lower scores, in turn, indicate greater risk.

An extremely low credit score, which suggests a history of poor debt management, may cause creditors to decide against lending you money, leasing you an apartment or issuing you phone or cable equipment. More often, lenders use credit scores, along with other information such as employment history and proof of income, to decide how much they are willing to lend you and at what interest rate. Landlords and utility companies also may use credit scores to help decide whether to charge you a security deposit—and how large it should be.

All other factors being equal, a higher credit score generally means you'll pay lower interest rates, fees and deposits. Over the lifetime of a loan, even a small reduction in rate can save you thousands of dollars in interest, so it pays to have a high credit score.

Credit Scoring Models

Credit scores are calculated using computer programs known as scoring models. Scoring models perform sophisticated statistical analysis on the contents of your credit report—your history of borrowing and repaying debts, as recorded by the three national credit bureaus: Experian, Equifax, and TransUnion. Scoring models look for patterns in your credit report data that historically have been associated with payment defaults among consumers. Based on the prevalence (or absence) of these patterns, scoring models assign you a score, usually in the form of a three-digit number, reflecting your predicted riskiness relative to other consumers.

Models developed by different companies, such as the FICO® Score* and VantageScore®, differ in how they calculate and report scores. There are also often multiple versions of a given model available from its developer (something like different versions of Windows or Android) and specialty models designed for specific industries. When comparing one credit score to another, or tracking changes in scores over time, it's important to know the following, to be sure you're making apples-to-apples comparisons:

- Which scoring model was used to calculate your score.

- The version number of that model.

- The highest and lowest scores you can get using that model (also known as the score range).

- Which credit bureau furnished the credit report from which the score was derived.

Whenever you receive a credit score, either from a creditor explaining a lending decision or when you check your own score for informational purposes, the law requires the inclusion of this information.

Credit Score Ranges

Trying to interpret a credit score without knowing its score range is a little like dressing to go outside when you're told the temperature is 30, but not whether that's in degrees Fahrenheit or Celsius. Knowing which scale to apply makes a huge difference. In that light, consider a credit score of 700.

As you'll see in more detail below, a score of 700 on the FICO® scoring range, which spans 300 to 850, indicates "good credit" and would likely make you eligible for a variety of loan offers. FICO® Scores are used in 90% of all lending decisions, so a FICO® Score is a pretty accurate reflection of your creditworthiness as a lender might see it.

The current credit scoring models from FICO® competitor VantageScore® Solutions LLC also use a score range of 300 to 850, but because VantageScore® models are calibrated differently from FICO® models, a score of 700 generated by those models (VantageScore® 3.0 or VantageScore® 4.0) is considered good verging on fair.

FICO® Auto Score Range

The FICO® Auto Score is a special variation on the FICO® Score designed for use in the auto financing industry and tailored to predict the risk of default specifically on car payments. FICO® Auto Scores are generated by making additional adjustments to standard FICO® Scores, but they use a different score range, of 250 to 900, with higher scores indicating lower risk.

FICO® Bankcard Score Range

The FICO® Bankcard Score is another industry-specific variation on the FICO® Score, customized for use by credit card issuers. It is fine-tuned to predict the risk of defaulting specifically on credit card payments. Like the Auto Score, the FICO® Bankcard Score uses a score range of 250 to 900, with higher scores indicating lower risk.

FICO® Scores and Mortgages

The vast majority of home mortgage lenders issuing new mortgage loans and refinancing existing mortgages use specific versions of the standard FICO® Score, with a score range of 300 to 850, when evaluating mortgage applications:

- FICO® Score 2 based on Experian data (also known as Experian/Fair Isaac Risk Model v2)

- FICO® Score 5 based on Equifax data (also called Equifax Beacon 5.0)

- FICO® Score 4 based on TransUnion data (also called TransUnion FICO® Risk Score 04)

These scoring models dominate the mortgage market because their use is required for all mortgages sold to Fannie Mae and Freddie Mac, the country's largest purchasers of residential home mortgage loans. Lenders who wish to sell mortgages to Freddie or Fannie use these FICO® models to meet Fannie and Freddie requirements.

What Is Good Credit, Anyway?

Lenders want borrowers who will repay their debts, on time and as agreed upon in a loan agreement. If a lender feels they can rely on you to do that, they say you have "good credit," or that you're a low-risk borrower. If based on a history of poor debt management, a lender doubts you will pay back a loan, they consider you to have "bad credit," and to be a high-risk borrower. Most consumers fall somewhere in the middle of that spectrum, and credit scores help lenders understand individual borrowers' level of credit risk.

Every lender has its own criteria for managing borrower risk. Some lenders avoid all but the lowest-risk borrowers, while others seek higher-risk borrowers with the understanding that they can charge them higher interest rates and fees as a trade-off.

Credit scores are a reflection of your credit history—of decisions (good and bad) you may have made about handling debt. The good news is that credit scores are not forever. They are snapshots of a moment in your credit history, and you can improve your credit score by making good credit decisions in the future. Good credit decisions today can lead to a more positive credit history in the future. That, in turn, can bring higher credit scores and better borrowing opportunities.

How Credit Scores Are Calculated

The specific calculations FICO® and VantageScore® use to generate credit scores are trade secrets, but their models all operate on the same data found in your credit report—all of which correspond directly to choices you make about borrowing and repaying the money.

Fair Isaac Corp., the maker of the FICO® Score, says the following factors matter most in its score calculations:

- Payment history. Paying bills on time helps your credit score. That's the single biggest factor, accounting for as much as 35% of your FICO® Score.

- Credit usage rate. Experts recommend using no more than 30% of your total credit card borrowing limit to avoid lowering credit scores. Credit usage, also known as your credit utilization rate, is responsible for about 30% of your FICO® Score.

- Length of credit history. FICO® Scores tend to increase over time. New credit users can't speed that up, but establishing a record of timely payments will help build scores as credit history stretches out. Length of credit history accounts for up to 15% of your FICO®Score.

- Total debt and credit. Credit scores reflect your total outstanding debt and the types of credit you use. The FICO® Score tends to favor a variety of loan types, including both installment credit (loans with fixed monthly payments) and revolving credit (like credit cards, with variable payments and the ability to carry a balance). Credit mix can influence up to 10% of your FICO® Score.

- Recent applications.Applying for a loan or credit card triggers a process known as a hard inquiry, in which the lender requests your credit score for use in its lending decision. Hard inquiries typically lower your credit score by a few points, but as long as you continue to pay your bills on time, scores typically rebound within a few months. (Checking your own credit is a soft inquiry and does not impact your credit score.) Recent credit applications can account for up to 10% of your FICO® Score.

- Derogatory information. Certain credit report entries can severely lower credit scores for extended periods of time, depending on the nature of the information. Because these entries are not found in all credit reports, FICO® doesn't assign them percentage weights. The negative impact of these entries dwindles over time, but initially at least, they can outweigh all other factors and severely drive down your credit score.

Derogatory entries include accounts sold into collections, foreclosures and bankruptcies.

VantageScore® scoring models evaluate credit using similar factors. VantageScore®characterizes their relative importance as follows:

- Most influential: Payment history (paying bills on time)

- Highly influential: Age and type of credit (establishing a good mix of loan accounts); percent of credit limit used (avoiding "maxing out" cards)

- Moderately influential: Total balances and debt (limiting debt to what's prudent)

- Less influential: Recent credit behavior and inquiries (applying for new credit); available credit (avoiding opening unneeded credit accounts)

Derogatory entries also severely impact VantageScore® credit scores, but the company's latest model, VantageScore® 4.0, ignores certain collections accounts related to medical debt.

While FICO® and VantageScore® differ somewhat on what factors matters most, credit scoring models are all trying to identify consumers who handle credit responsibly. If you adopt and stick with good credit habits, all of your credit scores will tend to improve.

Other Factors to Consider

- If you're a new credit user, you probably have a comparatively low credit score. That doesn't mean you've done anything wrong. It's just a reflection of lenders' desire for borrowers with a track record of responsible credit usage. As long as you pay your bills on time and avoid maxing out your credit cards, your score should increase steadily over time. There's not really anything that can be done to speed up the process, but you can derail it if you're careless, so be careful.

- Creditors almost never base lending decisions on credit scores alone. Depending on the type of loan and the amount you want to borrow, they may ask for proof of income, length of employment and even what savings and other assets you have, to gauge your ability to pay back the debt.

- Credit scores do not take into account income, savings, length of employment, or alimony or child support payments, but lenders may take these additional factors into consideration when making lending decisions.

Why Credit Scores Can Differ Between Experian, TransUnion, and Equifax

The three credit bureaus receive information about your credit usage in monthly reports from your lenders. The timing of those reports varies somewhat by the bureau and by the lender, which means the contents of your credit files at the bureaus are seldom identical. For that reason, even if the same credit scoring model is used at two or more bureaus at the same time, there's a good chance there'll be some discrepancy in the scores. Twenty-point differences are not unusual, and wider gaps are possible.

Recognizing this, some lenders request scores from two or even all three bureaus when they are considering credit applications. There are no hard and fast rules about this, but lenders who pull two scores often use the lower one in their decision-making, while lenders who pull three scores typically consider the middle score.

What Do Your Credit Scores Mean?

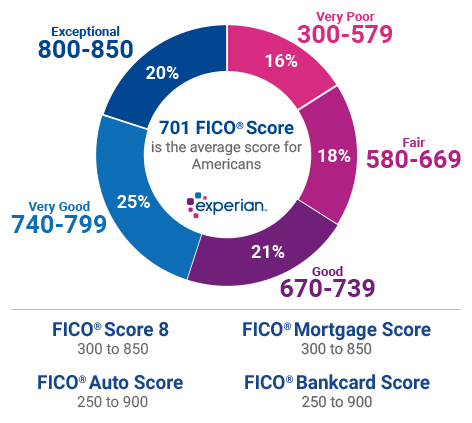

Because generic credit scores distill your history of credit usage and loan payment behavior into a single reference point, lenders often use them as one barometer of credit quality. Each lender sets its own standards, but here's a rough breakdown of how lenders view various groupings of FICO® Scores:

Exceptional: 800 to 850

FICO® Scores ranging from 800 to 850 are considered exceptional. People with scores in this range typically experience easy approval processes when applying for new credit, and they are likely to be offered the best available lending terms, including the lowest interest rates and fees.

Very good: 740 to 799

FICO® Scores in the 740 to 799 range are deemed very good. Individuals with scores in this range may qualify for better interest rates from lenders.

Good: 670 to 739

FICO® Scores in the range of 670 to 739 are rated good. This range includes the average U.S. credit score, and lenders view consumers with scores in this range as "acceptable" borrowers. People with scores in this range are likely to qualify for a broad array of loans and credit cards but are likely to be charged interest rates somewhat higher than the best available.

Fair: 580 to 669

FICO® Scores that range from 580 to 669 are considered fair. Lenders may disqualify individuals with these scores if they apply for mainstream loans. Consumers with scores in this range may be considered subprime borrowers, eligible only for loans with interest rates significantly higher than the best available.

Poor: 300 to 579

FICO® Scores that range from 300 to 579 are categorized as poor. Many lenders decline credit applications from people with scores in this range, which could be a result of bankruptcy or other major credit problems. Credit card applicants with scores in this range may only qualify for secured cards that require placing a cash deposit equal to the card's spending limit. Utilities may require customers with scores in this range to put down sizable security deposits.

Expand Your Range

Understanding where your credit score falls along the score range for the model that generated it is essential to making sense out of the score. It's also critical to any plans you may have for tracking and improving your score over time. With patience and perseverance, virtually anyone can improve their scores. Committing to avoiding late payments may be a good first step. Focusing on keeping card balances below 30% of their limits is another. And still another is checking the credit reports that underlie your credit scores.

You can check your credit reports from each of the national credit bureaus for free once each year, and that's a good habit to get into. Reviewing your credit report will let you know if there are any derogatory entries in your file—and indicate whom to contact to address them. In addition, checking your credit file will alert you to unauthorized credit activity that could be a sign of identity theft.

A better understanding of credit scores and the credit behaviors that determine them can help you move your score upward along the score range—to a better credit profile and greater borrowing options and opportunities.

Want to instantly increase your credit score? Experian Boost™ helps by giving you credit for the utility and mobile phone bills you're already paying. Until now, those payments did not positively impact your score.

This service is completely free and can boost your credit score fast by using your own positive payment history. It can also help those with poor or limited credit situations. Other services such as credit repair may cost you up to thousands and only help remove inaccuracies from your credit report.

Editorial Disclaimer: Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities. All information, including rates and fees, are accurate as of the date of publication.

This article was originally published on January 7, 2019, and has been updated.

*Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more.

https://www.experian.com/blogs/ask-experian/infographic-what-are-the-different-scoring-ranges/